-

Pl

chevron_right

Erlang Solutions: DORA Compliance: What Fintech Businesses Need to Know

news.movim.eu / PlanetJabber • 12 February 2025 • 7 minutes

The Digital Operational Resilience Act (DORA) is now in effect as of 17th January 2025, making compliance mandatory for fintech companies, financial institutions, and ICT providers across the UK and EU. With over 22,000 businesses impacted, DORA sets clear expectations for how firms must manage operational resilience and protect against cyber threats.

As cybercriminals become more sophisticated, regulatory action has followed. DORA is designed to ensure that businesses have the right security measures in place to handle disruptions, prevent data breaches, and stay operational under pressure.

Yet, despite having time to prepare, 43% of organisations admit they won’t be fully compliant for at least another three months. But non-compliance isn’t just a delay. It comes with serious risks, including penalties and reputational damage.

So, what does DORA mean for your fintech business? Why is compliance so important, and how can you make sure you meet the requirements?

What is DORA?

With technology at the heart of financial services, the risks associated with cyber threats and ICT disruptions have never been higher. The European Parliament introduced the Digital Operational Resilience Act (DORA ) to strengthen the financial sector’s ability to withstand and recover from these digital risks.

Originally drafted in September 2020 and ratified in 2022, DORA officially came into force in January 2025. It establishes strict requirements for managing ICT risks, ensuring financial institutions follow clear protection, detection, containment, recovery, and repair guidelines.

A New Approach to Cybersecurity

This regulation marks a major step forward in cybersecurity, prioritising operational resilience to keep businesses running even in the face of severe cyber threats or major ICT failures. Compliance will be monitored through a unified supervisory approach, with the European Banking Authority (EBA), the European Insurance and Occupational Pensions Authority (EIOPA), and the European Securities and Markets Authority (ESMA) working alongside national regulators to enforce the new standards.

A report from the European Supervisory Authorities (EBA, EIOPA, and ESMA) highlighted that in 2024, of the registers analysed during a ‘dry run’ exercise involving nearly 1,000 financial entities across the EU, just 6.5% passed all data quality checks . This shows just how demanding the requirements are, and the importance of getting it right early for a smooth path to compliance.

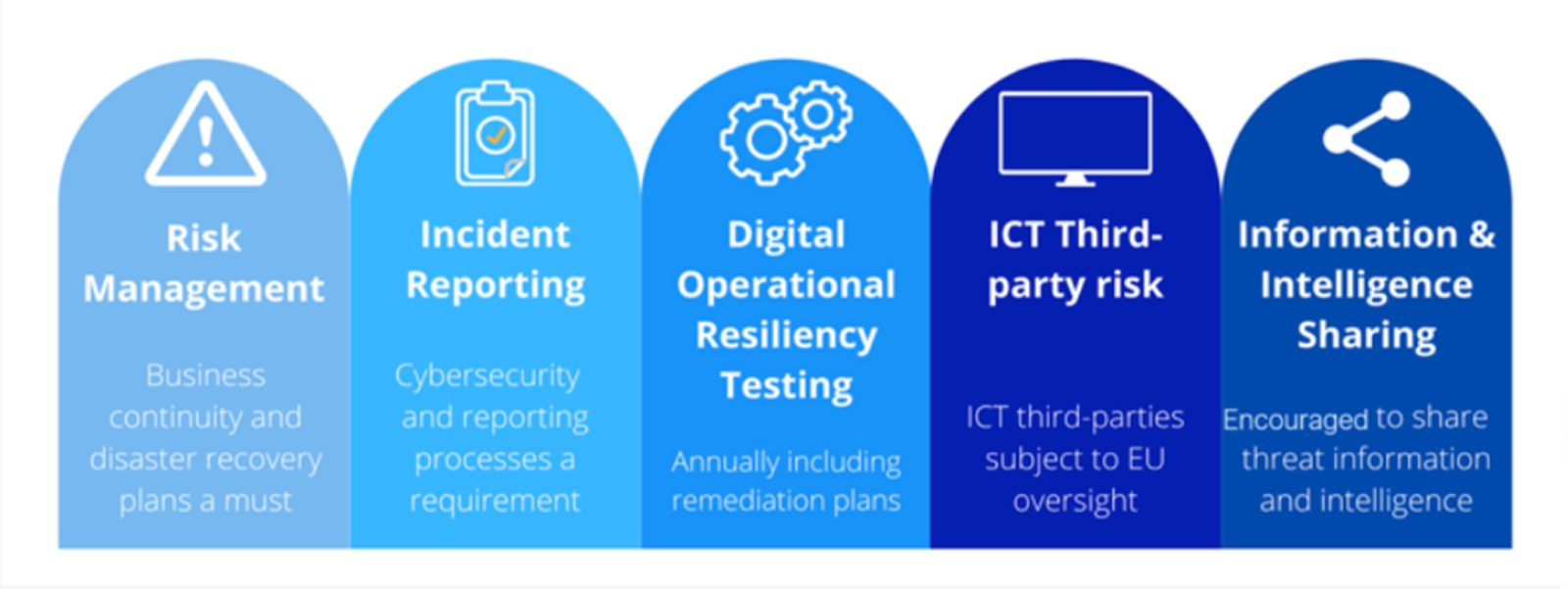

The Five Pillars of DORA

DORA introduces firm rules on ICT risk management, incident reporting, resilience testing, and oversight of third-party providers. Rather than a one-size-fits-all approach, compliance depends on factors like company size, risk tolerance, and the type of ICT systems used. However, at its core, DORA is built around five key pillars that form the foundation of a strong operational resilience framework.

Source: Zapoj

These pillars also serve as the basis for a DORA compliance checklist , which businesses can use to ensure they meet regulatory requirements.

Below is a breakdown of each pillar and what businesses need to do to comply:

1. ICT Risk Management

Businesses must establish a framework to identify, assess, and mitigate ICT risks. This includes:

- Conducting regular risk assessments to spot vulnerabilities.

- Implementing security controls to address identified risks.

- Developing a clear incident response plan to handle disruptions effectively.

2. ICT-Related Incident Reporting

Companies must have structured processes to detect, report, and investigate ICT-related incidents. This involves:

- Setting up clear reporting channels for ICT issues.

- Classifying incidents by severity to determine response urgency.

- Notifying relevant authorities promptly when serious incidents occur.

3. Digital Operational Resilience Testing

Financial institutions are required to test their ICT systems regularly to ensure they can withstand cyber threats and operational disruptions . This includes:

- Running simulated attack scenarios to test security defences.

- Assessing the effectiveness of existing resilience measures.

- Continuously improving systems based on test results.

4. ICT Third-Party Risk Management

DORA highlights the importance of managing risks linked to third-party ICT providers . Businesses must:

- Conduct due diligence before working with external service providers.

- Establish contractual agreements outlining security expectations.

- Continuously monitor third-party performance to ensure compliance.

5. Information Sharing

Collaboration is a key part of DORA, with financial institutions encouraged to share cyber threat intelligence . This may include:

- Participating in industry forums to stay informed about emerging threats.

- Sharing threat intelligence with peers to strengthen collective defences.

- Conducting joint cybersecurity exercises to improve incident response.

By following these five pillars, businesses can build a strong foundation for digital resilience . Compliance isn’t just about meeting regulatory requirements, it’s about safeguarding operations, protecting customers, and strengthening the financial sector against growing cyber threats.

How to Achieve DORA Compliance for Your Business

Regardless of the stage of compliance a business is in, there are a few key areas that must be focused on to protect themselves. Here’s what you need to do:

Understand DORA’s Scope and Requirements

The first step to DORA compliance is understanding what’s required. Take the time to familiarise yourself with its requirements and ask any questions.

Conduct a Risk Assessment

A solid risk assessment is at the heart of DORA compliance. Identify and evaluate risks across your ICT systems—this includes everything from cyber threats to software glitches. Understanding these risks helps you plan how to minimise their impact on your operations.

Create a Resilience Strategy

With your risk assessment in hand, develop a tailored resilience strategy. This should include:

- Preventive Measures : Set up cyber defences and redundancy systems to prevent disruptions.

- Detection Systems : Ensure you can quickly spot any anomalies or threats.

- Response and Recovery Plans : Have clear plans in place to respond and recover if an incident happens.

Invest in Cybersecurity and IT Infrastructure

To meet DORA compliance for business, invest in strong cybersecurity tools like firewalls and encryption. Ensure your IT infrastructure is resilient, with reliable backup and recovery systems to minimise disruptions.

Strengthen Incident Reporting

DORA stresses the importance of quick and accurate incident reporting. Establish clear channels for detecting and reporting ICT incidents, ensuring timely updates to authorities when needed.

Build a Culture of Resilience

Resilience is an ongoing effort. To stay compliant, create a culture where resilience is top of mind:

- Provide regular staff training .

- Regularly test and audit your systems.

- Stay updated on emerging risks and technologies.

Partner with IT Experts

DORA compliance can be tricky, especially if your team lacks in-house expertise. Partnering with IT service providers who specialise in compliance can help you meet DORA’s requirements more smoothly.

Consequences for Non-Compliance

We’ve already established the importance of meeting DORA’s strict mandates. But failing to comply with these regulations can have serious consequences for businesses- from hefty fines to operational restrictions. Here’s what businesses need to be aware of to protect their organisation:

Fines for Non-Compliance

- Up to 2% of global turnover or €10 million, whichever is higher, for non-compliant financial institutions.

- Third-party ICT providers could face fines as high as €5 million or 1% of daily global turnover for each day of non-compliance.

- Failure to report major incidents within 4 hours can lead to further penalties.

Reputational Damage and Leadership Liability

- Public notices of breaches can cause lasting reputational damage, affecting business trust and relationships.

- Business leaders can face personal fines of up to €1 million for failing to ensure compliance.

Operational Restrictions

- Regulators can limit or suspend business activities until compliance is achieved.

- Data traffic records can be requested from telecommunications operators if there’s suspicion of a breach.

How Erlang Solutions Can Help You with DORA Compliance

Don’t panic, prioritise. If you’ve identified that your business may be at risk of non-compliance, taking action now is key. Erlang Solutions can support you in meeting DORA’s requirements through our Security Audit for Erlang and Elixir (SAFE) .

With extensive experience in the financial sector, we understand the critical need for resilient, scalable systems. Our expertise with Erlang and Elixir has helped leading fintech institutions, including Klarna, Vocalink, and Ericsson , build fault-tolerant, high-performing and compliant systems.

SAFE is aligned with several key areas of DORA, including ICT risk management, resilience testing, and third-party risk management:

- Proactive Risk Identification and Mitigation : SAFE identifies vulnerabilities and provides recommendations to address risks before they become critical. This proactive approach supports DORA’s requirements for continuous ICT risk management.

- Continuous Monitoring Capabilities : SAFE allows ongoing monitoring of your systems, which aligns with DORA’s emphasis on continuous risk detection and mitigation.

- Detailed Incident Response Recommendations : SAFE’s detailed findings help you refine your incident response and recovery plans, ensuring your systems are prepared to quickly recover from cyberattacks or disruptions.

Third-Party Risk Management : The security audit can provide insights into your third-party integrations, helping to ensure they meet necessary security standards and comply with DORA’s requirements.

Conclusion

DORA compliance is now in effect, making it essential to act if your business isn’t fully compliant. Delays can lead to penalties and increased risk exposure. Prioritising ICT risk management, strengthening resilience, and ensuring proper incident reporting will bring you closer to compliance. But this isn’t just about meeting requirements, it’s about safeguarding your organisation and building long-term operational resilience.

If you have compliance concerns or just want to talk through your next steps, we’re here to help. Contact us to talk through your options.

The post DORA Compliance: What Fintech Businesses Need to Know appeared first on Erlang Solutions .